DCA vs lump sum — same amount, different result

When a chunk of money lands, the question follows — put it all in at once, or spread it out monthly. The same $12,000 lands differently in the two paths.

When a chunk of money lands, one question follows you around. "Should I put all of this in at once, or spread it out monthly?" Even with the same $12,000, buying the whole amount in one shot or buying $1,000 every month for 12 months produces different outcomes. Here's why the same total can produce different results.

What lump sum and DCA mean

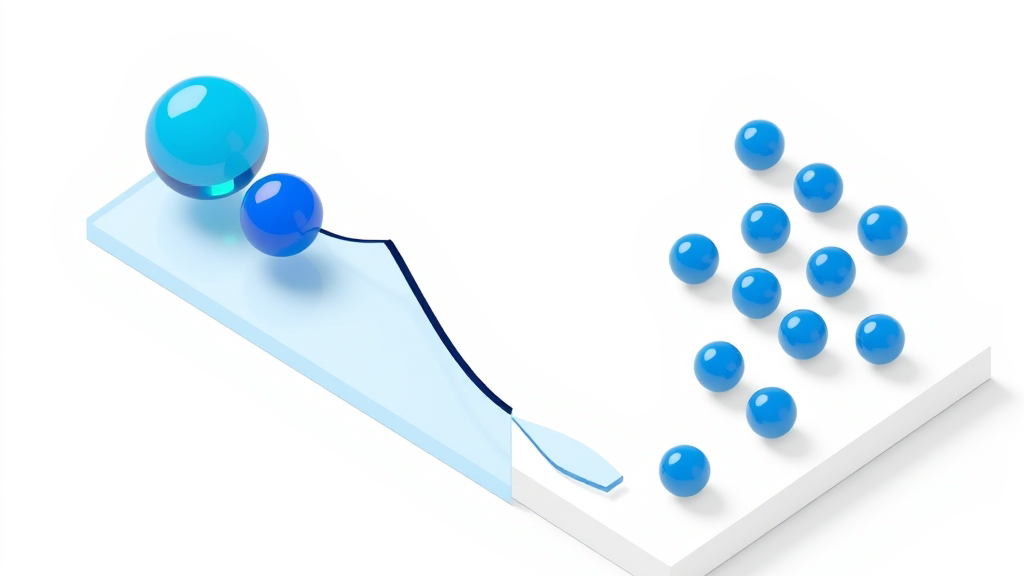

Lump sum means putting all the available money into the asset at one moment. With $12,000, the full amount goes into the purchase at a single point.

DCA (dollar-cost averaging) means buying the same amount split over a fixed schedule. The $12,000 becomes $1,000 each month for 12 months, or a fixed weekly amount, or a fixed daily amount.

Think of buying rice. Lump sum is buying a year's worth in one box. DCA is buying a bag each month. Same amount, different rhythm.

How they differ

The biggest difference is whether you carry the "when to buy" timing risk or not.

Lump sum makes one moment's price the reference. Cheap on that day and the start is good. Expensive on that day and the start is rough. The single purchase price becomes the entire curve's starting point.

DCA puts many moments into an average. Across 12 months of prices rising and falling, the average becomes your purchase price. A higher price on one day gets balanced by a lower price on another. That averaging effect is why DCA is often described in terms of "average cost smoothing."

Same total, different result

The same $12,000 in the same asset over the same period produces different outcomes. The market path during the window shifts the result.

In a steadily rising market, lump sum tends to come out ahead. With prices climbing throughout, buying the whole amount up front means more of it rides the climb.

In a market that dips deeply before recovering, DCA tends to come out ahead. Buying through the dip lowers the average cost meaningfully.

In a sideways market, DCA feels calmer. The full purchase price isn't locked at one point — many moments average together, so the swings hit less hard.

It isn't "lump sum is better" or "DCA is better." The shape of the market during the window decides. Running your own asset and period through both flows shows the difference in numbers right away.

Which one fits

If you knew which kind of market was coming, the answer would be obvious. No one knows in advance. So the fit usually comes from your own situation.

- A chunk lands and it makes you nervous → DCA is easier on the mind. If you'd lose sleep after putting it all in and watching the market drop, splitting it into 12 or 24 monthly slices removes a lot of weight.

- The market looks deeply discounted to you → lump sum fits. If the price already feels attractive, splitting the buys risks watching the price climb away while you wait.

- You invest from each paycheck → you're already doing DCA. Nothing to decide.

The point isn't to pick the right "when." It's to pick the flow you can actually stay with.

Looking at it directly

Running the same asset and period twice is the fastest way. Once as lump sum, once as DCA (daily, weekly, or monthly) with the same total and period. The two results land side by side, and the numbers settle the question.

One thing worth keeping in mind

The results are simulations built from past market data. Real accounts include trading fees, taxes, and slippage (small differences in execution price), which aren't reflected here. Under the same conditions, the actual return can come out lower than the displayed value.

For DCA specifically, more frequent purchases mean more accumulated fees in real accounts. The simulation doesn't capture that line, but a real account does.

Lump sum coming out ahead in the past doesn't mean it will in the future. Run both yourself and let the numbers help you find the flow that fits.

- This information is not investment advice.

- Past performance does not guarantee future results.

- Backtest results are simulations and may differ from actual trading outcomes.

Kistack is an information service designed to help users review market data independently and form their own judgments. These backtests are historical simulations based on public market data and do not guarantee future investment returns. Past performance is not indicative of future results. Trading costs such as fees, taxes, and slippage are not reflected in simulations. Data is provided by Kistack; decisions are made by users.

This information is provided for educational and informational purposes only and does not constitute investment advice within the meaning of the Investment Advisers Act of 1940 (IAA) §206. Kistack is not a registered investment adviser and does not provide individualized buy or sell recommendations.

All performance figures shown are historical simulations. Disclosures regarding past performance and risk are presented in a manner intended to be fair, balanced, and not misleading, consistent with FINRA Communications Rule 2210. No statement on this site is intended to omit material facts or to mislead readers under SEC Rule 10b-5 of the Securities Exchange Act of 1934.